I am not into budgeting as much, not because it does not help but because it is a chore. No one likes chores. And hence the many budgeting tools we find around us that help us seamlessly categorize our expenses to help find the problem areas.

But even that is an overkill, and I can attest to that. Because if we can get the big budget items right, the minor stuff hardly matters. That of course assumes that the minor stuff truly stays minor unless it turns into $100 lunches every other day.

Elizabeth Warren in her book All Your Worth that she co-wrote with her daughter, lays out the 50/30/20 budgeting framework that if adopted, could sort out most money problems from our lives. She is the same Elizabeth Warren who is a sitting United States Senator and remains a consumer finance champion for all of us. She is also the key reason why the Consumer Finance Protection Bureau as an entity exists. The CFPB as it is called is a highly effective agency that I have personally used several times to “rain” down on the abuse by banks and other financial institutions. Hope it stays around because the current madness in Washington wants it not to stay around which will be bad for all of us.

So, what is the 50/30/20 framework? It is about splitting our after-tax income into the needs, wants and save buckets and allocating our family expenses accordingly.

The needs bucket includes things like housing, transportation, food, insurance and utilities.

The wants is the money we spend on things like vacations, eating out, gadgets – all the stuff that we can reluctantly, yet easily curtail from our spending if the time comes.

The save bucket was not needed as much in the past as most had access to employer-provided pensions so saving for retirement was a done deal. Plus, retirement years were not as many. I mean folks did not live as long, which then reduced the need for a big savings bucket.

That is not the reality today. No one has access to pensions. We need to plan our own pensions. Plus, we are living longer. We will in fact spend more years retired than years working and hence the need to really save big.

And 20 percent is the bare minimum we must do if we want to have a chance at a comfortable retirement.

Putting some numbers behind that framework; say you make $100,000 a year so after taxes, you’d take home $70,000. And say you reserve half of that for the needs bucket. That is rough living in many of the jobs-rich parts of our country but then that is the way we have collectively decided to live so unless that changes, this will remain the unfortunate reality.

And our sprawl-dependent suburban living means we are required to spend money on cars instead of relying on public-transit or being able to walk or bike to work, school and stores but again, blame the city planners and the suburban way of life that is foisted upon us even if we want to choose otherwise. That is not counting the rest of the negative externalities around things like sprawl-induced climate change that will increasingly become a big factor in our lives.

And then there are the costs. Housing of course takes a big bite out of our monthly cash flow and everything costs more when one family lives on one piece of land that needs to be served with all the necessary infrastructure. Property taxes, maintenance and insurance are just the visible costs. Then there is the big opportunity cost for us and for society with all that productive wealth getting permanently parked into dirt.

Plus, excessive indulgence on homes is fraught with risks. We would never tie most of our savings to a single stock or a sector, but we do that all the time with housing, exposed to one local market in one geographical region with our fortunes rigidly tied to the economic ups and down of that region. Again, it is not our fault but that is how it has evolved to be.

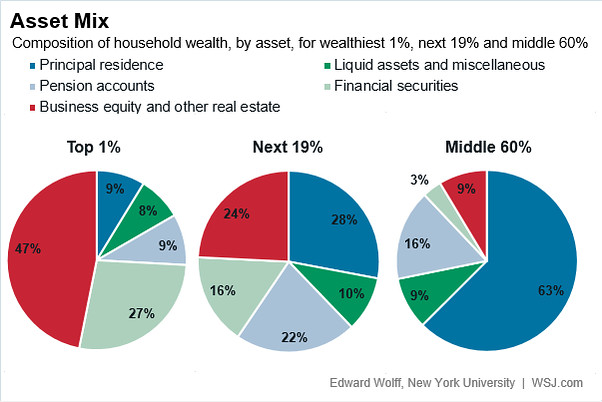

And one of the reasons the rich get richer is because they own most of the productive investments in the country. Data compiled by the Federal Reserve shows that the top 10% of Americans own 93% of all the publicly traded stocks. Where is most of the middle-class wealth? In homes because somehow the real-estate lobby has convinced us that homes are investments. They are not.

Granted, there is some bias in the data as it includes the likes of Bezos and Gates so quite naturally, their proportional wealth parked into their homes is tinier as compared to their stock holdings. But it is also obvious that the more of the means of production (businesses) you own, the wealthier you will be due to the way our economy works.

Back to the diatribe, since a car is a necessity, that is the next big cost we must pay for. How big is the damage? The Bureau of Transportation Statistics puts the annual car ownership cost at $12,000 on average which includes depreciation, maintenance and the rest. It does not yet include the biggest cost of them all and that is the opportunity cost of what else we could have done with that money were we not forced to spend it on owning and running a car. That is enough money to fully fund a great retirement if that cost didn’t exist through our working lives.

Talking about costs, I read a paper on how cities like Copenhagen and many others in the enlightened parts of the developed world greatly benefit by not having designed their cities around an auto-dependent way of life. And is it any wonder that these cities routinely rank as some of the happiest places to live?

Figures from the finance minister suggests that every time someone rides 1 km on their bike in Copenhagen, the city experiences an economic gain of 4.80 krone, or about 75 US cents. If that ride replaces an equivalent car journey, the gain rises to 10.09 krone per km, or around $1.55. And with 1.4 million km cycled every day, that’s a potential benefit to the city of between $1.05m and $2.17m, daily.

What makes Copenhagen the world’s most bike-friendly city?

Sean Fleming, World Economic Forum, October 5, 2018

Back to the budgeting framework, the needs budget already gets swallowed by the two biggest costs. That is not yet counting things like insurance, childcare etc. that we must spend money on.

But the money must come from somewhere so then it comes down to reducing our wants. So much for spending money on fun things in life.

But the 20 percent of the save bucket is something that we cannot skip on because no one is coming to the rescue to pay for our respective retirements.

And of course, that money cannot be sitting in bank accounts. We have got to put it to work or else we’d have a whole another set of problems. Not as bad as being broke but almost equally bad due to what inflation does to our savings over time.

So, 50 percent for needs, 30 percent for wants and then save the rest, at the minimum.

Thank you for your time.

Cover image credit – Mikhail Nilov, Pexels