Johnny Depp was once the highest paid actor with a net worth of $650 million1. In 2017, he filed a lawsuit against his business managers accusing them of stealing all his wealth and leaving him penniless.

His managers countersued claiming that Depp spent $2 million a month maintaining his lavish lifestyle that included spending $500,000 on rental warehouses, $200,000 on private jets and $3,000 a month on wine2.

No amount of money is enough when the expense side of the equation remains out of whack. And this is not the only story.

Back to the real world, say $50,000 is all you’ll spend each year in retirement. Income from Social Security is on top of that. And say you have got $2.5 million saved up. Is there a reason you should own anything but stocks?

Standard retirement planning advice states that as you get closer to retirement, you should own less stocks and more bonds because stocks are risky. That is how most target date funds work.

And with a less risky portfolio with bonds mixed in, you can confidently withdraw money from your accounts without ever running out.

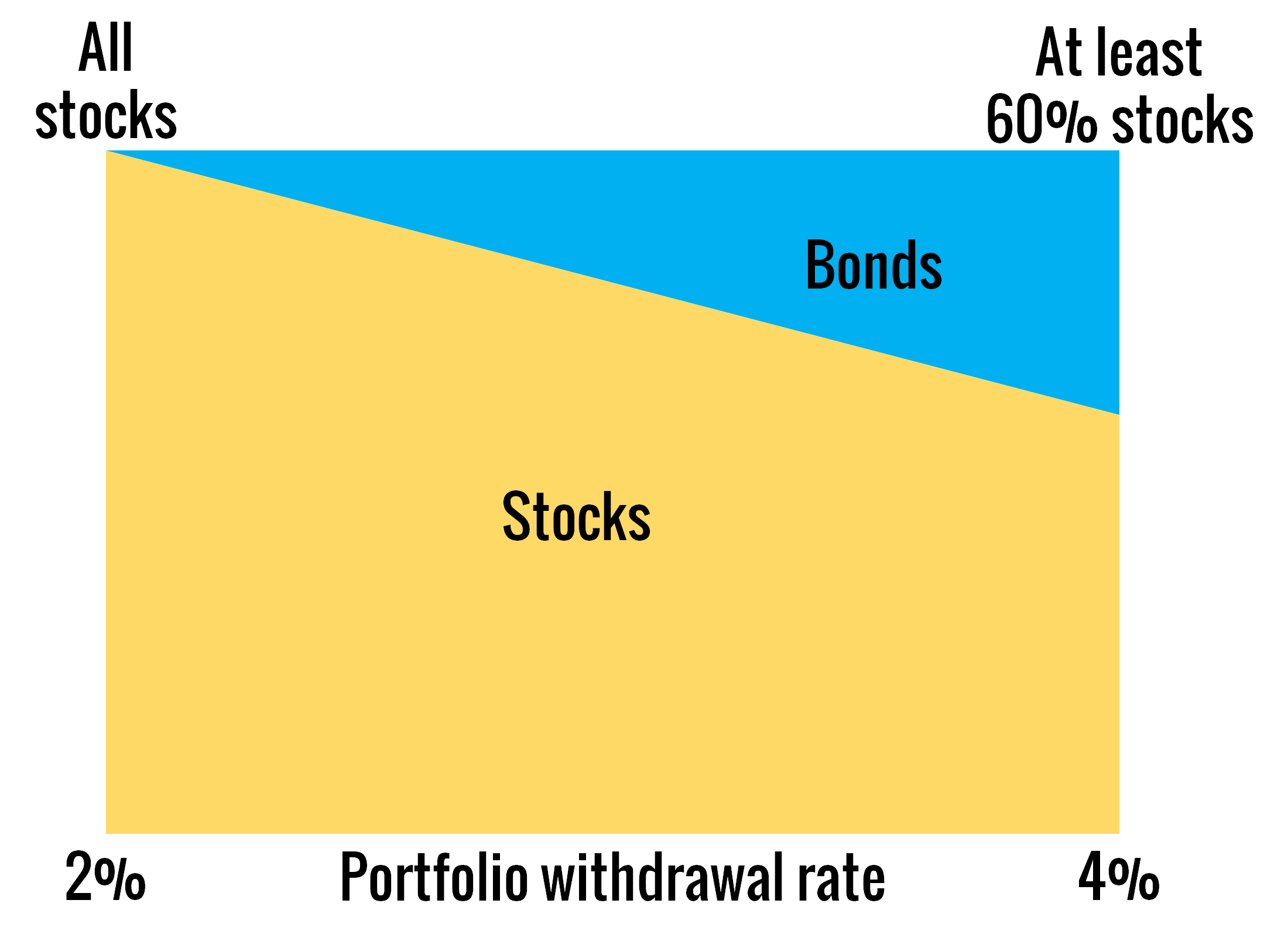

A 4% safe withdrawal rate has become the gold standard which means if you save up to 25 times your expenses (1/0.04 = 25), you are done.

Dividend yield on stocks these days is 2% so clearly, an all-stocks portfolio will run the risk of running out of money at a 4% withdrawal rate. Stocks are volatile and when you draw income from an all-stocks portfolio when they decline in price which they do from time to time, you won’t have much stocks left when their prices eventually recover.

Hence you mix in bonds that yield (interest income) more than stocks (dividends) to smooth out the ride.

But anytime you add bonds, you give up on growth, so you’ll end up with less when you are no longer around…if that matters to you. And you end up with less money when you add bonds to a portfolio because interest income from bonds is a cost to a business issuing those bonds. That business hence needs to earn more than its input costs or else it goes extinct.

The simplest way to think about it is with how the banking system works. Banks are in the business of lending money. They take our deposits and pay us interest. They then turn around and loan our deposits to borrowers at a higher interest rate than they pay us.

And if they don’t earn more than the interest they pay us, they cease to exist. The same logic applies to businesses who go out in the bond market and borrow money. If they don’t out-earn their interest expense, they cease to exist. Hence, it is structural for stocks to outperform bonds in the long run.

But say you have designed your happy life on $50,000 a year after accounting for income from Social Security and you have got $2.5 million in savings, do you then ever need to own bonds?

You don’t because $50,000 is 2% of $2.5 million that you can safely expect as dividends each year from an all-stocks portfolio.

Plus, dividends grow over time. In fact, the growth rate on dividends is designed to exceed inflation. Dividends are a portion of the profits that come back to you as a shareholder of the businesses you own and businesses are not in the business of losing money.

So, when input costs for a business rise due to inflation, it has two choices – either absorb those costs without raising prices for the stuff they sell and slowly wither away or pass down those costs to their end customers while preserving their profit margins.

Businesses in aggregate tend to do the latter and hence dividends continuing to outpace inflation in the long run makes sense. And the data proves that3.

But an all-stocks portfolio is going to be way more volatile than a balanced mix of stocks and bonds but that only matters if you make it matter.

Risk and return are inextricably intertwined. In almost every country where economists have studied securities returns, stocks have had higher returns than bonds. Further, if you want those high stock returns, you are going to have to pay for them by bearing risk; this is a polite way of saying that in the course of earning those higher returns, your portfolio is going to lose a truckload of money from time to time. Conversely, if you desire perfect safety, then resign yourself to low returns. It really cannot be any other way.

William Bernstein

But what about real estate? First, you’ve got plenty exposure to real estate if you own a home.

Second, by being owners of corporations that make up the stock market, you already have a sizable implicit exposure to real estate through real estate investment trusts and through direct ownership of physical real estate these corporations own. Take McDonald’s for example. A fifth of its market value is derived from the physical ownership of real estate that it leases to its franchises.

And last, just like interest on bonds, the rent or the mortgage you pay is also an indirect cost to the businesses you own through the stock market. The company has to pay you enough in your paychecks to enable you to live wherever the company decides to create that next job and still clear profits.

If it cannot, it will not be creating that job which then reduces demand for real estate and eventually denting their prices.

So back to drawing income from your savings, if the size of your savings can help you sustain on a 2% withdrawal rate, you can choose to own an all-stocks portfolio and depart this planet with lasting generational wealth.

But if you need more income, then you’ll need to own bonds. Income from Social Security is like owning an inflation-indexed annuity (guaranteed income for life) so I wouldn’t go overboard with bonds. The guideline below is what I recommend and of course, it varies based on individual circumstances.

In short, if you are rich, you are set 🙂 – rich not just in terms of having great possessions but rich in terms of having fewer wants.

Thank you for your time.

Cover image credit – Tima Miroshnichenko

1 Stephen Rodrick. “The Trouble With Johnny Depp“, MarketWatch. June 21, 2018.

2 Eriq Gardner. “Johnny Depp Settles Blockbuster Lawsuit Against Business Managers“, The Hollywood Reporter. July 16, 2018.

3 Mark Hulbert. “You need to pay more attention to dividends — this math shows why they beat inflation“, MarketWatch. April 23, 2022.