Your identity will never be stolen – until it does. And once your thing is out there, it’s a mess.

You thought you cleaned it up and then it pops up again. Millions fall victim to identity theft. You don’t want to be them.

And we can get insurance against identity theft using precautionary measures below. All for free.

Checking your credit profile often

There are three bureaus who track your data – Experian, TransUnion and Equifax. You can check your credit files for free at each one of these sites as many times as you want. I do it once a quarter. I think that’s plenty.

There are also apps like CreditKarma that give you real-time access to your credit files. For free again.

Freezing your credit files

Freezing access to your files is the best defense against identity theft. It takes a bit of work but freezing your files is easy. You’ll have to do it at all three bureaus though. And it should be free. If you get asked for money, you are looking at the wrong thing.

But once your credit files are frozen, you are done. No new credit can be taken out without you thawing your files. You can then freeze your files again.

Credit bureaus don’t like it when you freeze your files, but the system has left you with no choice.

And the next time anyone wants to run your credit, find out which bureau they use and thaw your file there. And then freeze it again.

Don’t leave a trace

I shred everything. I’ll buy a good cross-cut shredder and keep it running.

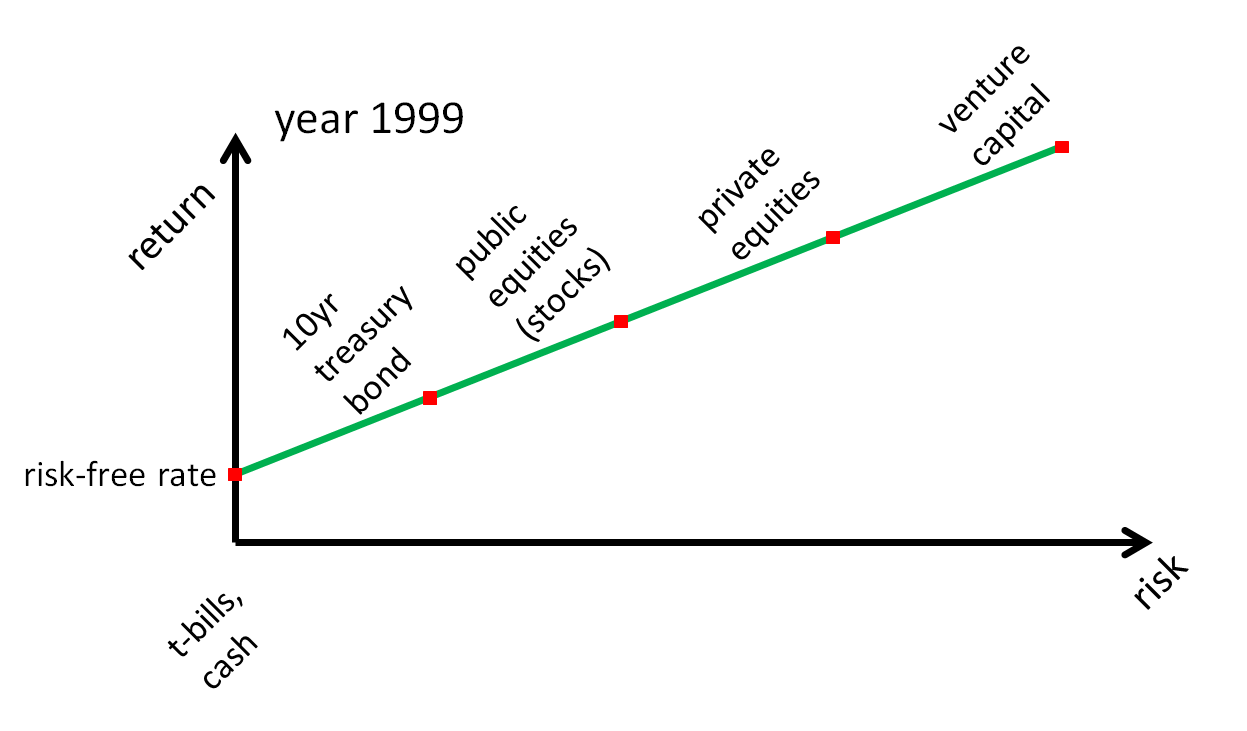

Treasury bonds are issued by the federal government. Bonds with a maturity of one year or less are called Treasury bills but we’ll keep calling them bonds.

So, say the year is 1999 when one-year Treasury bonds paid 4 percent as interest. If bonds with a maturity of one year paid 4 percent, you would naturally expect more payment from a five-year Treasury bond. Five years is a long time to wait to get your money back.

The five-year bond hence must pay like 6 percent else why would you take the risk of locking up your money.

And if the five-year Treasury bond pays 6 percent, same maturity corporate bond must pay higher. Corporations cannot print money, but governments can. Corporations carry that extra risk of going bankrupt.

Following along that risk spectrum, we would demand an even higher interest rate from an issuer of the same maturity junk bond, also called a high-yield bond. This is the investment world’s attempt at putting lipstick on a pig but do not be fooled by the pleasant sounding high-yield term. Junk bonds are issued by businesses that are on the verge of going out of business.

The riskier the issuer of a bond hence and/or the longer the time to maturity of that bond, the higher the rate of return. That is expected and that is how it usually goes. That describes the universe of bonds.

And if bonds yield whatever they yield, publicly traded stocks must yield more. Stocks are riskier than bonds because cash flows (dividends) from stocks are not guaranteed. And in the event of a bankruptcy, stockholders come last in line on any claims on business assets. So, stocks in theory should earn more than bonds.

If public stocks yield whatever they yield, venture investments must yield even more. We have to discount cash flows from venture-backed investments at a much higher discount rate than those for established, publicly traded businesses. That is a roundabout way of saying that we should expect a higher rate of return from venture investments than other types of investments because they are the riskiest.

The risk-return relationship just described is the Capital Markets Line and it looks something like this…

Treasury bills (risk-free rate) are the shortest maturity and the safest of all investments. Venture capital is the longest maturity and the riskiest of all investments.

And we’ve probably heard that the more risk we take, the more return we’ll earn.

But if riskier investments could be counted upon to deliver higher returns, by definition, they wouldn’t be any riskier. The prices of those investments would be bid up to a point where no net return above the risk-free rate exists. So, the higher risk equals higher return theory does not quite hold.

The correct way to formulate the Capital Markets Line then is…

We now have a distribution of returns instead of point estimates. The riskier an investment, the wider the distribution of return outcomes.

Howard Marks in his book, The Most Important Thing talks a great deal about this and more but this one quote captures the essence of the reconstituted Capital Markets Line…

The correct formulation is that in order to attract capital, riskier investments have to offer the prospect of higher returns, or higher promised returns, or higher expected returns. But there’s absolutely nothing to say those higher prospective returns have to materialize.

Howard Marks

Prospect, promised, expected mean the same. Investments that are riskier must appear to offer higher returns. They don’t necessarily have to deliver on that promise though.

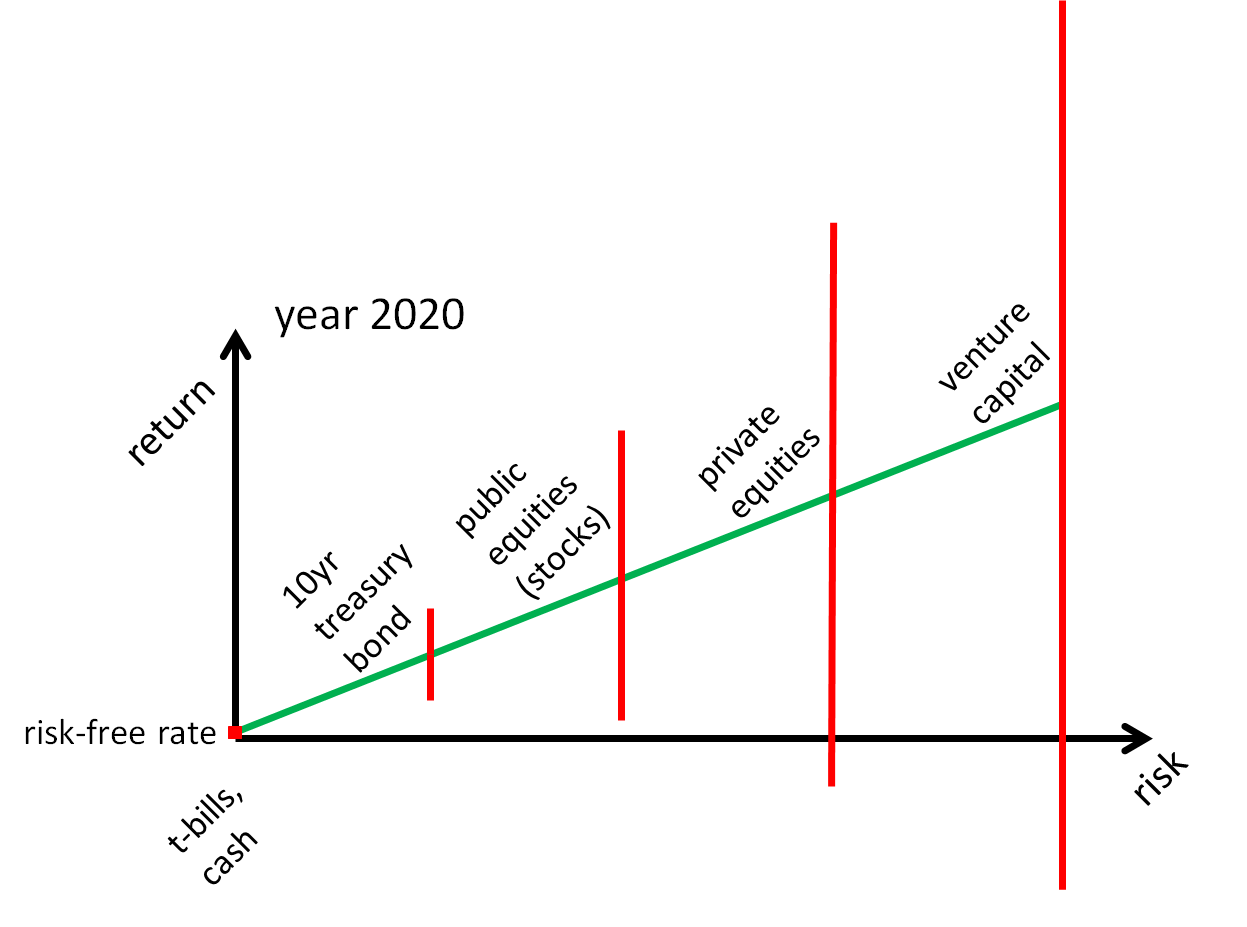

So that was the world of 1999.

Then we had some interim booms and busts so the Federal Reserve, in their attempt to make sure the economy doesn’t collapse, floored the interest rates.

The updated Capital Markets Line following that…

The entire line shifted down, which means the discount rates (expected rates of return) for each one of those investments moved down as well.

And when discount rates go down, investment values go up. The 4 percent bond you own now is more valuable when market interest rates are zero.

But when market interest rates rise again, we start to go back to the 1999 interest rate regime which then means discount rates rise and consequently, investment values fall. Projects and businesses that were flourishing in the low interest rate world suddenly don’t pencil out. Because the hurdle rate now is no longer zero.

But then your future expected return on any new money you deploy is higher. The time to invest is when investment values are low and expected returns are high. That is counter to how we behave but that is human nature doing what it always does.

Berkshire Hathaway class A shares trade at hundreds of thousands of dollars. This below is the price for each share…

Apple shares trade at hundred and some dollars apiece.

And the shares of Uber trade at a twenty plus dollars.

So, Uber stock is cheaper than Apple stock and Apple stock is cheaper than Berkshire Hathaway stock?

Of course not.

A ten-dollar stock is not cheaper than a hundred-dollar stock. A hundred-dollar stock is not cheaper than a thousand-dollar stock. A thousand-dollar stock is not cheaper than a million-dollar stock.

To understand why, we start with market capitalization. I’ve highlighted that in red above along with the P/E or the price over earnings ratio for each of the businesses shown.

Market capitalization (market value) of a publicly traded business is its stock price times the number of shares that are outstanding.

Market capitalization = Stock price x Number of shares outstanding

Apple’s market value as of the date of this post is about two trillion dollars. So, if you wanted to buy the whole of Apple as a business, you’ll need to come in with that much money.

How many Apple shares are out there in the market? That is the market capitalization divided by the stock price so about 16 billion shares.

Apple can decide tomorrow to split its shares and give you ten shares for each of the shares you own. What will that do to its stock price? It will drop by a factor of ten.

What should that do to the market value of Apple? Nothing except for some dumb reason, people think they are getting a deal so demand for the shares rise and so does the price. That is just noise, and the price eventually settles down to the true value. The demand for shares does not always rise so if you think you’ve found some secret to make money upon knowing that a stock is about to split…you haven’t.

Now we get to valuation. Wish life was that easy but the price to earnings ratio is the first thing you go to get a feel of how much return are you getting for each of your investment dollars. Berkshire trades at a price to earnings ratio of eight (7.89) so its earning yield which is the inverse of P/E is 12.5 percent.

The same yield for Apple is 4.5 percent, so not quite as good of a deal as Berkshire.

And Uber has never made money because it does not have a price to earnings ratio yet.

So, Berkshire even when it trades at hundreds of thousands of dollars a share is in fact a bargain compared to Apple and Apple a much better bargain compared to Uber.

I know and hopefully you know that that is a very simplistic view on valuation, but you get the point. Stock price in and of itself does not mean anything. It is the market capitalization and how much profit a business makes in relation to that market capitalization that decides whether a business is trading at a bargain or not.

And in this day and age when you can buy fractional shares, the price of a stock means nothing.

Crypto is not an investment. It can never be an investment. The United States dollar is not an investment. The Japanese yen is not an investment. The Euro is not an investment. None of these are investments. They are all currencies.

The latter ones at least are.

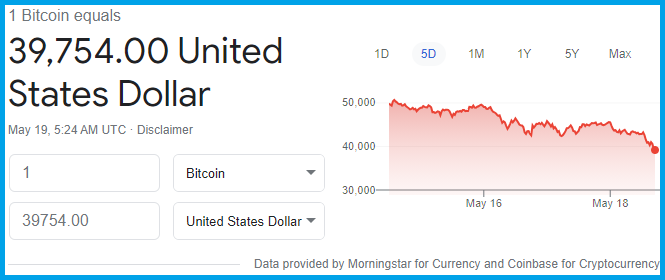

Crypto is not even a currency. Anything that does this…

…with one tweet from Elon Musk can never be a currency.

That’s on bitcoin. And of course, the hate from the cultists follow.

Most cults end badly, especially the ones that involve money.

It’s amazing to watch something come out of nowhere and get to a point where bitcoin trades at today. Because it’s a work of complete fiction. There are no cash flows with bitcoin. There is no intrinsic value.

And there apparently are thousands of such cryptocurrencies as of the date of this writing1.

So, what is to say that something better would not come along and replace the ‘utility’ that bitcoin supposedly provides today. There is no proven utility of bitcoin yet in its decade-plus years of existence.

Cryptos could become a medium of exchange someday but mediums of exchanges are not investments.

Bitcoin is the epitome of survivorship bias. We all know about it because it is the most popular and the most ‘successful’ of all cryptocurrencies.

But just because bitcoin has done whatever it has done does not mean it was a good investment. It was never an investment.

And there is no reason why it could not have turned out like this…

From hundred dollars to zero in weeks.

All cryptocurrencies will eventually find a similar fate. They are literal Ponzi schemes. There is nothing justifying their prices except that you must find a Greater Fool who’ll buy them from you at prices higher than what you paid for them.

Cryptocurrencies only seem to “work” when prices are going up. On the way down, nothing functions as it should – a trait common to Ponzi schemes throughout history.

And the heartaches and the agonies that unfortunately follow the implosions of Ponzi schemes…

At their height, luna and UST had a combined market value of almost $60 billion. Now, they’re essentially worthless.

The entire episode has laid bare the advantages of experienced large-scale investors over retail investors gambling on hope.

One person posted on Reddit that they didn’t think they would have enough money to pay for their next semester at school after losing money on luna and UST. Another investor affected by the crash tweeted that she and her husband sold their house and bet it all on luna, noting that she was still trying to digest whether it was actually happening or just a nightmare.

Others are contemplating suicide after losing all they’ve got.

“I’m lost, about to commit suicide in a chair,” one commenter posted to Reddit. “I lost my life savings in the investments of (LUNA UST) the worst thing is that 3 weeks ago I proposed to my girlfriend. She doesn’t know anything, I lost 62 thousand dollars. I’m here I don’t know what to do.”

The linked CNBC piece above is a must read if you want to know what truly goes on behind the scenes. While the trying-to-get-rich-quick John Q public was loading up on Luna, the schemers and the promoters were quietly dumping their wares on to them – a classic pump and dump scheme with tattoos and all.

And Do Kwon, the main schemer behind the creation of cryptocurrency Luna weeks before the collapse…

Can you ever imagine a Buffett or a Bogle behaving like this?

And if crypto is your investment thesis to get you from where you are to your goals, there is no thesis. It’s a gamble. It’s Vegas money without the Vegas fun.

Don’t sleep-walk through life playing these random games and hoping things will pan out. Because soon you’ll be 60 and wondering where your time and money went.

And did I make it clear that cryptocurrency is a giant Ponzi scheme? Maybe I didn’t but Sohale Andrus Mortazavi writing for Jacobin surely did.

Economist Hyman Minsky once wrote that stability brings instability. The more stable things become, and the longer things remain stable, the more unstable the system gets until an eventual crisis hits.

And it makes sense. When there is never a risk in sight, when everyone is fat and happy is when the chances of the risk showing up are the highest. Bad loans get made. Misallocation of capital is rampant. Businesses that should not exist, exist.

Bear markets that usually precede recessions are a required process to weed out those excesses. They are normal. They help capitalism thrive. And they must intermittently happen.

There is no technical definition for a bull market because no one complains when stocks are going up. But a bear market is when stocks go down 20 percent or more. Why 20 percent, we don’t know, and we don’t care.

But bear markets allow us to buy businesses that are temporarily on sale. We own businesses through stock ownership.

And the longer-term trajectory of the value of global businesses is up. It must be up. We all go to work for our respective employers each day, every day to make them more money today than we did for them yesterday, last month and last year.

So as owners of these businesses, we are bound to profit from the collective efforts of millions of our fellow beings, who toil day in and day out to better our world and make us money in the process.

So spread your savings wide and deep and keep on dollar-cost averaging into your plan. No one can consistently predict when bear markets come but they eventually end. They will end.

My first exposure to a stock market boom and bust cycle was back home in India in the early 1990s in what was deemed the ‘Harshad Mehta’ scam. It was a classic pump and dump scheme that was financed by fake bank receipts which Mr. Mehta’s firm brokered in transactions between banks. He used the money in the interim to pump up junky Indian stocks, wait for everyday folks to follow him into buying them and then sell at once, crashing their prices. He of course walked away with a boatload.

And everyone was ‘playing’ the market. The game was to buy these pieces of paper, watch their prices rise, sell, and get rich. Free money.

That party ended when the scam was uncovered. Many got wiped out. Blue-chip stocks suffered big declines.

And as it is with any big boom and bust cycle, the regulators would want to put the blame on someone. There were many to blame, including that uncle who wanted to get rich quick but then flamboyance has its costs. Harshad Mehta became an easy target. He was arrested and later died in prison at age 47, a sad end to an otherwise very clever personality.

But that was the early 90s and here we are today, and this is what a diversified portfolio of Indian stocks did since then…

That time in red with prices hugging the zero line, that was the Harshad Mehta scam.

And there were many more booms and busts since then but any money in the Indian stock market made you rich. Dividends were plenty. Tax incentives were bountiful.

The second boom and bust cycle that I intimately remember was the internet mania of the late 1990s. And luckily for me, I had no money to invest.

But that was a thing. I mean there was so much money flowing through the Silicon Valley economy that a person I knew with no intention of buying a car, goes out for lunch, test drives a high-end sports car and comes back from lunch with that car. True story, I swear.

There was so much money flowing through the Silicon Valley economy that a machine operator who worked two jobs to make ends meet, starts work at one of those jobs and walks away with stock options worth a million dollars eight months into it. True story, I swear.

The name of the game then…

It became a joke that the dot-coms that started out promising a grand vision of a more efficient way of doing business were — almost to a company — unprofitable. It’s entirely possible that a lot of them could have focused on the very real efficiencies that selling online made possible, and thereby slowly grown into sustainable businesses. But that was not the name of the game in the late nineties.

The venture capitalists who backed these companies were aiming for supernova IPOs because that’s when they got paid. Any IPO meant an exit for venture investors. Those incredible first-day “pops” that dot-com stocks experienced when IPOing? That was the early money cashing out, selling their shares to the investing public. The dot-com bubble was a fantasy period when a lot of VCs actually didn’t careif a business turned a profit, because it didn’t need to. “We’re in an environment where the company doesn’t have to be successful for us to make money,” a venture capitalist at Benchmark admitted when mulling over a pre-IPO investment in Priceline.

The bubble eventually burst. Then there was so much money flowing out of the Silicon Valley economy that a person I knew, goes to a work conference with a $6.4 million portfolio on Monday, and comes back from that conference to a $1.3 million portfolio that same week. True story, I swear.

There was so much money flowing out of the Silicon Valley economy that many I knew who were about to retire had to start over.

The third monster boom and bust cycle I got to experience was of course The Great Recession of 2008. This quote by the then President George W. Bush towards the tail end of that episode said it all…

If money isn’t loosened up, this sucker could go down.

That sucker was the global financial system and our literal way of life.

And you can read all you want about that time, but you had to live through it to truly know how it felt. The stock markets would drop and drop and drop for months at end with no sign of a recovery.

Yet you had to invest because it was the best time to invest. Charlie Munger calls this the process of inversion where you invert a situation to make peace with how you decide to act.

So back to that sucker, say it did go down, then it did not matter whether you invest or not.

But if the sucker did not go down, then you’ll come out at the other end far richer.

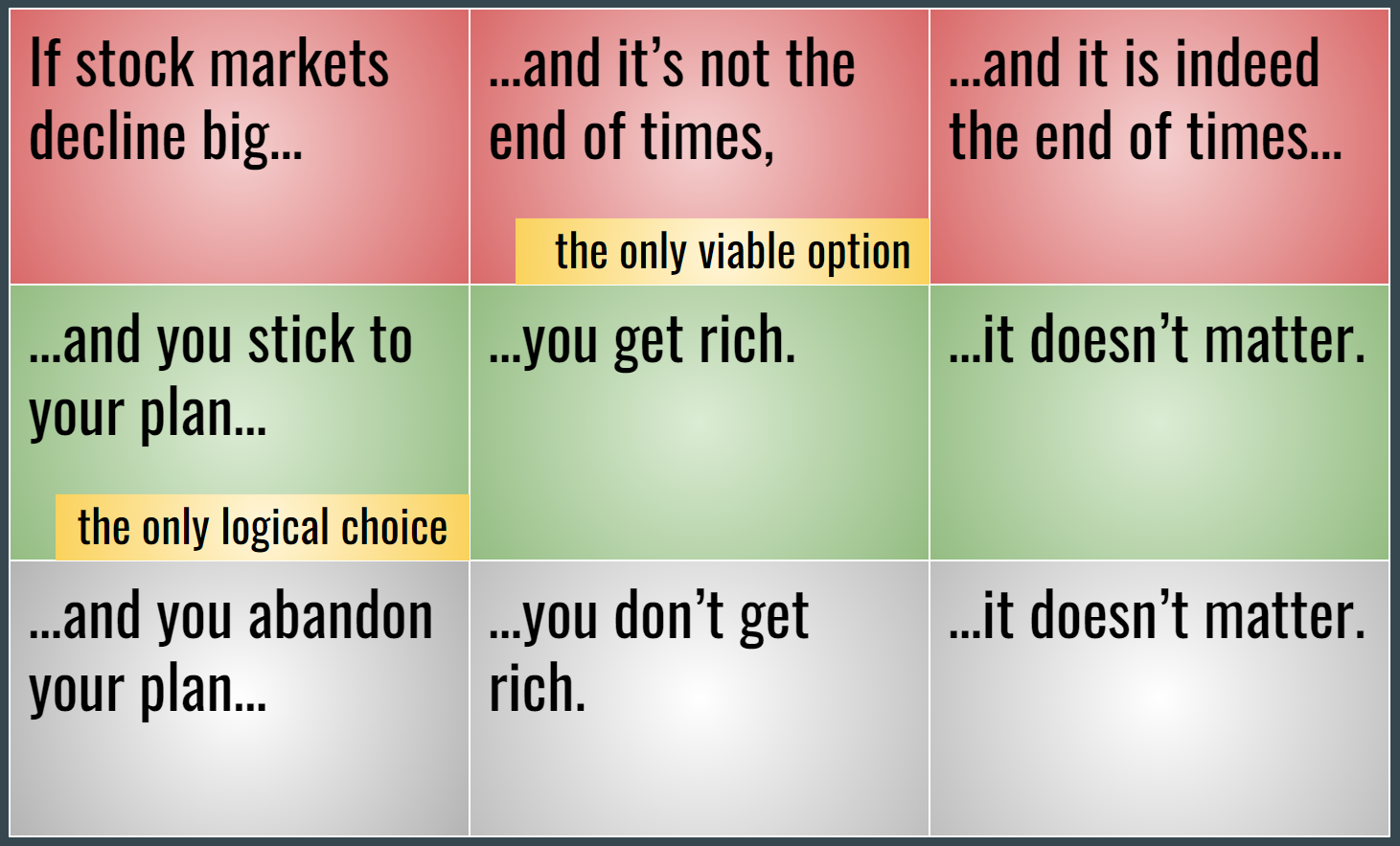

Blaise Pascal, the 17th century French mathematician posits that if you had to wager on the existence of God, which side should you bet on? That decision making quandary, called the Pascal’s Wager, explained…

If God is not, whether you lead your life piously or sinfully is immaterial. But suppose that God is. Then if you bet against the existence of God by refusing to live a life of piety and sacraments, you run the risk of eternal damnation; the winner of the bet that God exists has the possibility of salvation. As salvation is clearly preferable to eternal damnation, the correct decision is to act on the basis that God is.

An excerpt from one of the best books on understanding risk, Against the Gods by Peter Bernstein

The Pascal’s Wager version for our money…

So, during times of market mayhem, you stick to your plan and it is not the end of times then you get rich. There is no other option.

Large market declines are normal because market is made of people and people go crazy from time to time.

If you’re not willing to react with equanimity to a market price decline of 50% two or three times a century you’re not fit to be a common shareholder and you deserve the mediocre result you’re going to get compared to the people who do have the temperament, who can be more philosophical about these market fluctuations.

Charlie Munger

And when they do, remind yourself of Pascal’s Wager and invest away.

If you are into weight training, you know that if you want to increase muscle mass and strength, you must lift heavy. Heavy to a point of discomfort. Heavy to a point of pain. Not that I would know but that is what I’ve heard.

The same applies to investing. You must be willing to endure occasional discomfort and sometimes pain on this journey to financial independence.

And unless you are doing something crazy with your money, most of that pain relates to plain vanilla asset price volatility.

So, what determines an asset’s price? But before that, what is an asset? Or to be even clearer, what is an investable asset?

An asset is anything you own. But for an asset to be investable, it must produce cash flows or have the prospect of producing cash flows.

A painting is not an investable asset. The car you own, though considered an asset, is not an investable asset. The gold jewelry you own is not an investable asset. Cryptos, NFTs and anything that anyone cooks up and brings to the market with never any prospect of producing cash flows are not investable assets.

A share in a business on the other hand is an investible asset. So is a bond issued by that business. The home you own is an asset. They all directly or indirectly produce cash flows or have the prospect of producing cash flows.

And what determines an asset’s price? Take that share in a business you own that trades on a stock exchange. Millions of market participants at any given time are crunching their own numbers and their collective opinions about that business’s value gets reflected in its share price we see quoted on that exchange.

The quoted price is mostly right but not always. That is knowable only in hindsight. In the long run though, the price and the value of that asset will converge. And we should invest with that in mind.

Talk about valuing an asset, the basic building blocks are the same, be it a stock or a bond or real estate and this is how we derive its value. We first estimate an asset’s future cash flows. And since we hate waiting for those cash flows to hit our bank or brokerage accounts right away, we value them less the longer we have to wait.

That is, we devalue or discount the cash flows that arrive way out in the future more than the ones that show up say, next year.

We’ll use valuing a stock as an example.

Though inherently simple, there is a lot going on here. Ignoring the book value (the value of buildings, machinery etc.) of a business to make the math simple, stocks as we know are long duration assets. They are perpetuities in theory with cash flows expected to go on forever. That is what the three dots at the end signify. The cash flows continuing forever is not true for every stock but for a portfolio of stocks, that assumption should hold true.

And by design, stocks are ideal as long-term investments. You don’t start a business and expect it to turn a profit next year.

So, every time you put new money into your 401(k), you are indirectly providing capital to a new or existing business to try something new, to explore a better way of doing the old thing, to invest in research and development that someday finds cure for cancer, to make us into a space faring civilization etc. etc.

All that takes time.

So, don’t go near the stock market expecting a return in a year. In fact, don’t go near it if you expect something out of it in less than five years.

But back to the valuation model, the D is the first year cash flow (dividend). Stocks eventually in some form or the other pay out all the accumulated profits back to the shareholders in the form of dividends.

And as the profits generated by the businesses you own grow, the dividends grow and that is captured by the dividend growth rate, r.

Then there is the discount rate, i. Discount rate is many things. It is the opportunity cost of what else could you have done with the money that you are using to buy stocks. Discount rate hence is the return you expect from your investments.

But your return in a way becomes the cost of capital for those businesses. Safe, blue-chip businesses have lower discount rates and hence a lower cost of capital. A start-up on the other hand, has a higher discount rate and a much higher cost of capital.

Plus, when you think of opportunity cost, you also need to think about risk. Dividends are not certain. The growth rate of those dividends is not certain as well.

And depending upon the type of business you own, the certainty of dividends and the certainty around the growth rates of those dividends vary.

Johnson & Johnson is in a different league of dividend payers than say, Juniper Networks. Which one would we ascribe a lower discount rate to? Johnson & Johnson of course because it is deemed safer with predictable dividends.

And discount rate being in the denominator means for the same set of cash flows, we’ll ascribe a higher value to Johnson & Johnson as a business than Juniper Networks.

A bit more on opportunity costs. It is one thing to be gung-ho on stocks when bonds pay nothing. Because there are not many viable options to invest your savings. That has been the world for so long that we have a hard time imagining there could be alternatives.

But when interest rates on super-safe Treasury bonds rise, now we have choices. Why would we invest in stocks when Treasury bonds yield say 8 percent with zero risk. That is not to say that we are there yet, but you get the point.

So, the discount rate, even for Johnson & Johnson rises when interest rates rise. And when discount rates rise, the value of a business falls.

Some takeaways hence…

If you are starting out, the fastest way to get to a net worth of $100,000 is through increased income via career growth or entrepreneurship and not through investment returns. The same applies if your net worth is under a million dollars. Markets will do whatever they’ll do but the two things you can control are how much you make and how much of what you make, you can save. The rest is all noise. So, focus on where you can make the biggest difference.

Investment superstars come and go but mean reversion is here to stay. Do not be enamored by anything or anyone that has shot the lights out of what normal investing should normally yield. If the risk-free rate is 5% and you earn 30% on an investment, do not be shocked when that eventually mean reverts. Free lunches are few and far between.

Never, ever, ever, ever, never, ever be completely in or out of the markets. All it takes is 5 minutes of Googling to realize that market timing has never worked and will never work. The only thing you can and should do is adapt your plan to what your gut can handle. It is one thing to fill out a risk tolerance questionnaire and assume that you can handle double-digit declines in your portfolio’s value. It is an entirely different ball game when you are experiencing it. So, take notes and implement changes when necessary.

Naval Ravikant, the founder of AngelList, says that investing favors the dispassionate. That is, markets tend to efficiently separate emotional investors from their money. So don’t let Mr. Market take advantage of your anxiety, greed and fear. The only way to get around that is through a well-crafted investment policy statement customized for your plan. And then when Mr. Market goes through its usual manic-depressive phase, you go revisit that plan to see if changes are necessary. If not, sit tight and don’t peek.

Of course, think long term. John Bogle, the founder of Vanguard, once said that the daily machinations of the stock market are like a tale told by an idiot, full of sound and fury, signifying nothing. Nothing about the businesses you own changes much from one year to the next. Capitalism is here to stay and business ownership is where the bulk of the riches lie. Either you can be a cog (worker) in that wheel or own a piece of that wheel. Own that piece at every chance you get.

And last, there are three ways to go broke, a la Charlie Munger – liquor, ladies and leverage. No comments on the first two but leverage will eventually kill. It works like a charm when all is going well and then you go broke overnight. Use it sparingly.

Reserves as in safe. Reserves as in accessible. Reserves as in durable.

There is nothing safer than cash. There is nothing more accessible than cash. And if done right, there is nothing more durable than cash.

And by done right means that the quantity of reserves matches the duration required of those reserves.

For most, that duration is three to six months’ worth of living expenses. That is not gross income, that is not net income but expenses. You need that many months of expenses set aside to tide you through in case things go bad.

Situations like rental property ownership might require more in reserves but for many, three to six months of expenses set aside is plenty.

Any cash beyond that belongs in investments. It must or inflation will slowly and then suddenly chomp away at your hoard. That is compound interest working in reverse.

On where to park those reserves, a high-yield savings account will continue to remain an ideal place as immediate access to cash is needed.

But I prefer a better option and that is buying Series-I savings bonds. The “I” in Series-I stands for inflation-indexed which means you get to preserve the long-term purchasing power of your money.

And it gets better as there are two parts to the interest you earn on these bonds:

The fixed-rate part which remains fixed for the life of each new bond you buy.

The inflation-indexed part which changes twice a year (in May and in November) based upon latest inflation data.

And both parts that make up the interest income get automatically reinvested until you redeem (sell) the bonds or when the bonds mature (in 30 years). This is compound interest working for you.

No state or local income tax on the interest earned, ever.

No Federal income tax until the bonds are redeemed or mature.

That is all super but there are some catches:

You only get to buy up to $10,000 worth of these bonds for each person, each year. Bring in a partner and we are talking $20,000 annually. I consider that plenty in a given year

Once you buy these bonds, you will not be able to redeem them for the first 12 months.

And if you do redeem them before the 5-year anniversary of the purchase date of each new I-bond, you forfeit the last three months of interest as penalty.

But assuming you can plan around these inconveniences, I would do the bond buying for a few years between you and your partner and that is all the emergency stash you’ll ever need.

But there is another interesting take on these that I’ll personally employ if I were say a decade away from retiring. This is of course surplus cash beyond fully funding your plan that you get to use and purchase insurance to protect against something called the Sequence of Returns risk.

Sequence of Returns risk is retiring into a particularly bad phase in the markets so if you happen to retire into one, you can draw down this bond buffer while you wait for the markets to recover.

Buying these bonds, or any bonds for that matter, is not a get rich quick scheme. The right kind of bonds, which I-bonds happen to be, protects your purchasing power while insuring against the risk I just described.

And regardless of what anyone says, insurance is an expense. You give up on growth buying these bonds instead of say investing in the stock market.

You can buy these bonds at treasurydirect.gov. You’ll need another account for your partner.

But back to the essence of maintaining reserves, get to that stash first before doing anything else. That of course assumes you don’t carry any debt but if you do, extinguish that first before getting to the reserves.

Say someone you know is running short on funds and comes to you for a loan that he promises to pay back in a month. Will you lend him the money? And if so, would you do it for free?

You’d say why not. You have loaned him money before and without fail, he pays you back on time.

But say that same someone comes to you for a loan that he promises to pay back in a year? Would you loan him the money for free then?

It is different this time, isn’t it? Money loses value over time due to inflation so waiting a year means you are losing purchasing power.

And now say he comes to you for a loan that he will pay back in 10 years? The risk now just went up manyfold.

The longer the duration, the greater the chance you will not see your money back and hence, the greater the risk. And the greater the risk, the higher the interest rate you will demand on your loan.

That same thing plays out in the bond market. When you lend money, you are in fact buying a bond regardless of whether you are lending it to a friend, to a government or to a business. They do have different risk profiles as they should but inherently, it is the same thing.

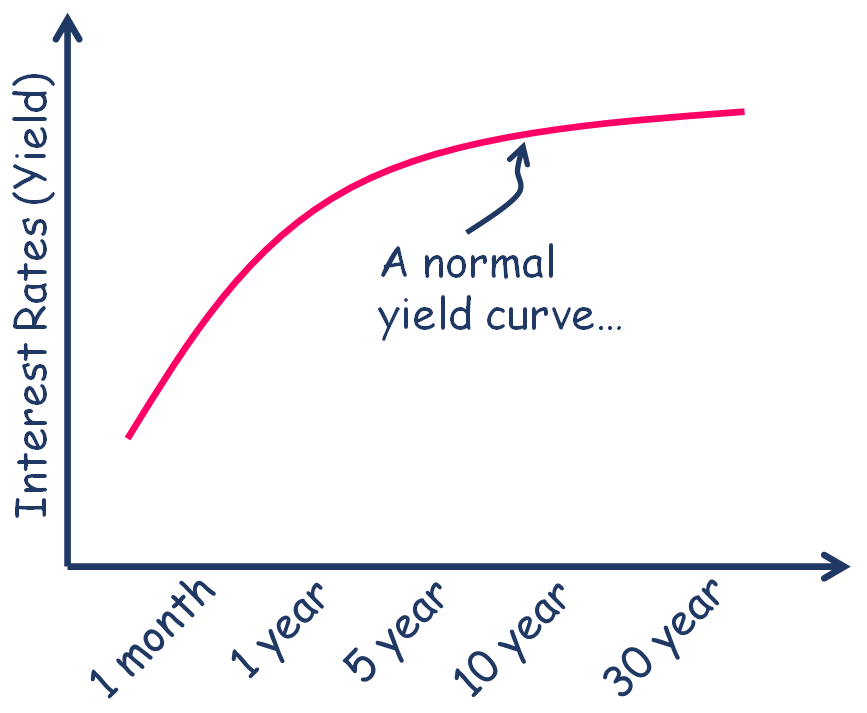

United States Treasury bonds are the safest of all bonds you can buy. They range in maturity from 30 days to 30 years. A bond matures when the loan term ends.

So, between say a 30-day bond versus a 30-year bond, which one do you think should pay a higher interest rate?

The 30-year bond, of course.

A lot can happen in 30 years whereas not much usually happens in 30 days. By investing in a 30-year bond, you are giving up access to your savings for a much longer duration, hence a much greater risk.

And in return, you’d demand a higher interest rate.

So, interest rates gradually slope up as bond durations rise. That is the yield curve, and it makes intuitive sense.

Now if yields on short duration bonds rise while yields on long duration bonds remain unchanged and they rise to a point where now both the short and the long duration yields are the same, that is a flattish yield curve. It does not make logical sense that that should ever happen, but it does sometimes.

But when the short duration bond yields rise to a point where now they are higher than the long duration ones, that is an inverted yield curve.

But that does not make sense. Why would a yield curve flatten or invert?

We hear about the Federal Reserve raising or lowering interest rates and we think they control all interest rates.

But they only control the overnight rates that they charge banks for the use of the money. That duration is only a day so that is the shortest of the short end of the yield curve.

Longer term rates like what we pay for mortgages and car loans are at the mercy of the markets, their expectations of growth rates and inflation.

And the Federal Reserve does not care much about the shape of the yield curve. All its charter is to make sure that the economy has full employment and stable prices.

That is, the Fed wants anyone looking for a job to be able to find one while ensuring that inflation remains tame, and deflation never takes hold. And they engineer that by manipulating the overnight rates they charge banks.

When unemployment is low, but inflation is raging, the Federal Reserve will act to slow things down and they do that by raising the cost of borrowing. Raise short-term rates with no impact on the longer-term rates and the yield curve flattens. And that can lead to a recession, so investors naturally get concerned.

But recessions are part and parcel of a healthy economic cycle. No one can predict their timing though but nothing about your long-range financial planning should change with whatever is happening to the yield curve.

Because yield curve changes are temporary while your investment timeframe is almost permanent.

A widely known way to value a stock is its price to earnings ratio. It tells us what investors are willing to pay for each dollar of profit a business behind that stock earns.

The other way to look at that same information is by flipping that ratio upside down. That is, earnings divided by price or the earnings yield.

That is your yield today when you own that stock.

That earnings yield must be greater than a similar duration but safer investment or else why would you invest in that stock?

Stocks as we know are ownership stakes in businesses and their aggregate value depends upon profits and the growth rate of those profits.

And profits are unpredictable. They may come. They may never come.

So, there are risks with stock ownership and you want to get compensated for taking on those risks. And hence the equity risk premium.

But premium over what?

Stocks are long duration assets which means you must wait a while for profits to flow back to you on your investment.

So, when you decide to invest in stocks, you’d want to compare that against a similar duration and of course a safer benchmark investment. And the safest of them all that matches an aggregate stock market’s approximate duration is the 10-year Treasury bond.

So, you’d want to compare the yield on the 10-year Treasury bond with the earnings yield of your stock or better yet, a basket of stocks.

That extra yield that stocks earn over bonds is the equity risk premium you expect to earn. That is the market compensating you for taking on the risk of investing in businesses.

And depending upon what is going on in the economy at any given time, that risk premium can change.

Coming out of traumatic economic times and you’ll see some of the widest risk premiums and the best of times to invest.

When everyone is fat and happy, stupidly making money is when the risk premiums are the narrowest. And those usually are the worst times to invest.

But come to think of it, everything and anything to do with making investment decisions, almost everything boils down to that 10-year Treasury bond yield. It is like a linchpin that guides all capital allocation decisions – in your home, at your business and with your investments.

The lower that yield, the lower the discount rate. The lower the discount rate, the lower the hurdle rate and the more bloated everything becomes.

And when that yield changes to the upside, everything gets a reset…to the downside.